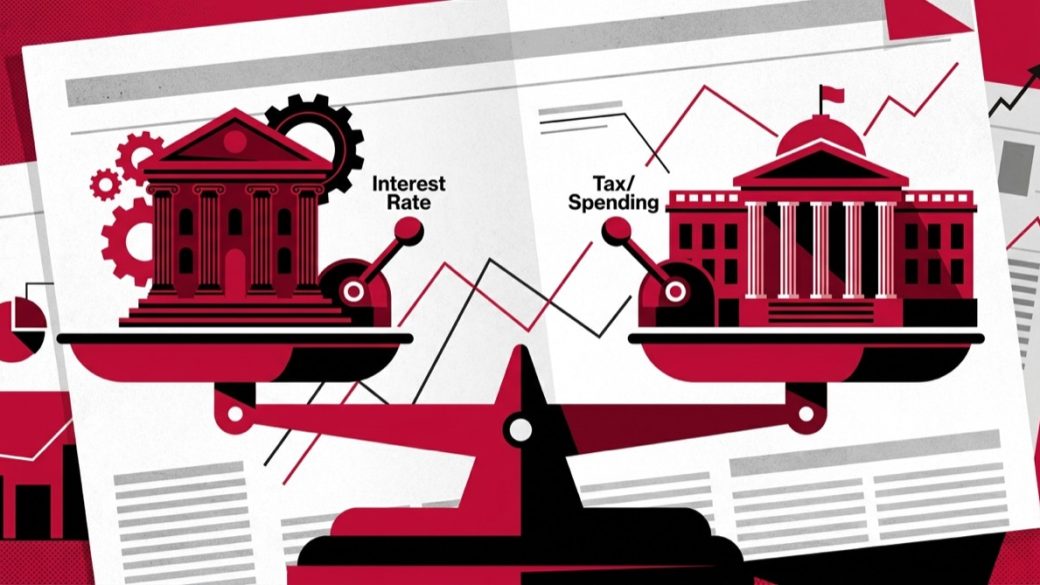

Monetary policy is how the Reserve Bank of India (RBI) manages the cost and supply of money — mainly by moving interest rates like the repo rate — while fiscal policy is how the central government manages its taxing and spending through the Union Budget. Both aim to keep growth steady and inflation in check, but one is run by the central bank and the other by the Ministry of Finance.

What “economic policy” actually means

An economy is just millions of people and businesses buying, selling, borrowing, saving and investing. Left entirely alone, it tends to swing between booms (when spending runs hot and prices rise too fast) and slumps (when demand dries up and jobs disappear). Economic policy is the set of deliberate decisions the state uses to smooth out those swings — to support growth and employment while keeping prices reasonably stable.

In almost every modern economy, including India’s, this job is split between two arms that pull different levers:

- Monetary policy — controls the price and quantity of money in the system. In India this is the domain of the central bank, the RBI.

- Fiscal policy — controls what the government taxes and what it spends. In India this is the domain of the elected government, executed through the Union Budget.

Think of the economy as a car. Monetary policy is the accelerator-and-brake on the cost of borrowing; fiscal policy is the government deciding how much fuel to buy and which roads to build. Used well, the two work together. Used carelessly, they can cancel each other out. The rest of this guide breaks down each lever, how they differ, and how India actually steers between them.

Monetary policy: the RBI and its toolkit

Monetary policy is the process by which the central bank influences how much money is available in the economy and how expensive it is to borrow. In India, this responsibility sits with the Reserve Bank of India, which derives its powers from the Reserve Bank of India Act, 1934.

The legal mandate: flexible inflation targeting

Since a 2016 amendment to the RBI Act, India follows a flexible inflation targeting (FIT) framework. The central government, in consultation with the RBI, sets a numerical inflation target. The current target is 4% Consumer Price Index (CPI) inflation, with a tolerance band of +/- 2 percentage points — meaning the RBI aims to keep retail inflation between 2% and 6%. This target is reviewed every five years.

If inflation stays outside the 2–6% band for three consecutive quarters, the RBI is legally required to write a report to the government explaining why it missed the target and what it will do to fix it. That accountability is a defining feature of the modern framework.

Who actually sets the rate: the Monetary Policy Committee (MPC)

Interest-rate decisions are not taken by the Governor alone. They are taken by the Monetary Policy Committee (MPC), a six-member body created by the 2016 amendment:

- Three members from the RBI — the Governor (who chairs the committee), a Deputy Governor in charge of monetary policy, and one official nominated by the RBI Board.

- Three external members appointed by the central government.

Each member gets one vote, and decisions are by majority. In the event of a tie, the Governor has a second, casting vote. The MPC meets at least four times a year (in practice, usually six bi-monthly meetings) and publishes the minutes, so the public can see how each member voted and reasoned.

The RBI’s main tools

The RBI does not print and hand out cash to control the economy. Instead it nudges the banking system using a set of established instruments:

| Tool | What it is | How it works |

|---|---|---|

| Repo rate | The rate at which the RBI lends short-term funds to commercial banks. | The headline policy rate. Cut it and loans get cheaper; raise it and borrowing slows. This is the lever most often in the news. |

| SDF / reverse repo | The rate the RBI pays banks to park surplus funds with it. | Helps absorb excess cash from the system and sets the floor of the rate corridor. |

| CRR (Cash Reserve Ratio) | The share of deposits banks must keep as reserves with the RBI. | Raising CRR locks up money banks could otherwise lend; lowering it frees up lending capacity. |

| SLR (Statutory Liquidity Ratio) | The share of deposits banks must hold in safe assets like government bonds. | Another dial controlling how much banks can lend versus must hold. |

| Open Market Operations (OMO) | RBI buying or selling government securities in the market. | Buying bonds injects money into the system; selling bonds pulls money out. |

| MSF / Bank rate | The penal rate at which banks borrow against emergency limits. | Sets the upper edge of the rate corridor for overnight funds. |

Expansionary vs contractionary monetary policy

Monetary policy broadly runs in one of two modes:

- Expansionary (easy) money: When growth is weak or the economy needs support, the RBI cuts rates and adds liquidity. Cheaper loans encourage businesses to invest and households to spend.

- Contractionary (tight) money: When inflation is running hot, the RBI raises rates and drains liquidity. Costlier loans cool demand and bring price rises back under control.

Fiscal policy: the government’s taxing and spending

Fiscal policy is the use of government revenue (mainly taxes) and government expenditure (spending) to influence the economy. In India, the headline event for fiscal policy is the Union Budget, presented in Parliament by the Finance Minister, traditionally on 1 February each year.

The two halves: revenue and spending

Every fiscal decision falls on one of two sides of the ledger:

- Taxation (money in): The government raises revenue through direct taxes (income tax on individuals, corporate tax on companies) and indirect taxes (most importantly the Goods and Services Tax, or GST, plus customs duties). Cutting taxes leaves more money in people’s hands; raising them does the opposite.

- Expenditure (money out): The government spends on capital expenditure (capex) — long-lived assets like highways, railways, ports and defence — and on revenue expenditure — salaries, pensions, interest payments and subsidies. More spending injects demand into the economy.

The fiscal deficit and borrowing

When the government spends more than it earns, the gap is the fiscal deficit, which it finances by borrowing (largely by issuing government bonds). A deficit is not automatically bad — borrowing to build productive infrastructure can lift future growth — but persistent large deficits raise interest costs and can crowd out private borrowers.

To keep this in check, India has the Fiscal Responsibility and Budget Management (FRBM) Act, 2003, which commits the government to a disciplined, transparent path for the deficit and public debt. In recent years the government has emphasised bringing the fiscal deficit down as a share of GDP over the medium term.

Expansionary vs contractionary fiscal policy

Like monetary policy, fiscal policy has two gears:

- Expansionary fiscal policy: Cut taxes and/or raise spending to boost demand — typically used during slowdowns. This widens the deficit.

- Contractionary fiscal policy: Raise taxes and/or trim spending to cool an overheating economy or repair the deficit.

One useful idea is the automatic stabiliser: even without any new announcement, tax collections fall and welfare spending rises automatically in a downturn, gently supporting the economy; the reverse happens in a boom.

Monetary vs fiscal policy: the core difference

Both policies try to manage the same thing — the overall level of demand in the economy — but they differ in who runs them, what tools they use, and how quickly they act. Here is the side-by-side:

| Feature | Monetary policy | Fiscal policy |

|---|---|---|

| Run by | The RBI (central bank), via the MPC | The central government / Ministry of Finance, via the Budget |

| Main tools | Repo rate, CRR, SLR, OMO, liquidity operations | Taxes (income tax, GST), government spending, borrowing |

| Primary goal | Price stability (the 4% +/- 2% inflation target), supporting growth | Growth, employment, redistribution and public services |

| Decision speed | Fast — the MPC can change rates at a scheduled meeting | Slower — major changes usually wait for the annual Budget and Parliament’s approval |

| Accountability | To the inflation mandate; reports to government if it misses | To Parliament and ultimately to voters |

| Affects you via | EMIs, fixed-deposit returns, loan availability | Tax rates, subsidies, public investment, jobs |

How the two policies interact

Monetary and fiscal policy are not rivals — they are two hands that work best when coordinated. But they can also pull against each other.

When they work together

In a deep slowdown, the most powerful response is for both arms to pull in the same direction: the government spends more and cuts taxes (expansionary fiscal) while the RBI cuts rates and adds liquidity (expansionary monetary). India’s response to the COVID-19 shock of 2020 is a textbook case — large government relief and capital-spending packages alongside sharp RBI rate cuts and extraordinary liquidity support.

When they pull apart

Tension appears when the two arms disagree about the cycle. If the government runs a very large deficit (pumping demand in) while the RBI is trying to fight inflation (pulling demand out), the central bank may have to keep rates higher for longer to offset the fiscal push. Heavy government borrowing can also push up bond yields, raising borrowing costs across the economy — the “crowding-out” effect.

The bridge: government borrowing and the RBI

There is a practical link between the two. The RBI acts as the government’s debt manager, conducting the auctions through which the government borrows. The RBI’s open-market operations (buying and selling those same government bonds) influence both liquidity and bond yields. So even though the two policies are run by different institutions, they meet in the government securities market.

| Economic situation | Typical monetary response | Typical fiscal response |

|---|---|---|

| Recession / weak growth | Cut repo rate, add liquidity (easy money) | Cut taxes, raise spending (wider deficit) |

| High inflation | Raise repo rate, drain liquidity (tight money) | Trim spending, raise/keep taxes; target deficit |

| Steady, on-target economy | Hold rates, keep a neutral stance | Focus on quality of spending and deficit path |

Real Indian examples

Monetary policy in action

The clearest example is the RBI’s repo-rate cycle. When retail inflation climbed well above the 6% upper band in 2022, the MPC moved into tightening mode and raised the repo rate over successive meetings to bring inflation back toward target. As inflation eased, the committee shifted to a more accommodative footing and began lowering rates to support growth. Each move directly changed the EMIs on millions of home and auto loans — the most personal way monetary policy reaches households.

Fiscal policy in action

On the fiscal side, the government’s sustained push on capital expenditure in recent Union Budgets — sharply higher allocations for roads, railways and infrastructure — is expansionary fiscal policy aimed at crowding in private investment and lifting medium-term growth. On the revenue side, the introduction of GST in 2017 was a structural fiscal reform that reshaped how indirect taxes are collected across the country.

Who decides what?

It is easy to mix up the institutions. Here is the clean division of labour in India:

- Monetary policy → the RBI. Specifically, the six-member Monetary Policy Committee sets the repo rate and the policy stance. The RBI also manages liquidity, CRR/SLR and open-market operations. Its anchor is the inflation target set jointly with the government.

- Fiscal policy → the central government. The Ministry of Finance designs the Budget; Parliament debates and approves it. Taxes, spending and the borrowing plan are political decisions answerable to voters.

The inflation target is the one place the two formally meet: it is set by the government in consultation with the RBI, and then the RBI is left operationally independent to hit it. This separation — political control over fiscal choices, central-bank independence over interest rates — is considered good practice worldwide because it keeps day-to-day money decisions insulated from short-term political pressure.

Frequently asked questions

What is the difference between monetary policy and fiscal policy?

Monetary policy is run by the RBI and works by changing the cost and supply of money — mainly the repo rate, plus tools like CRR, SLR and open-market operations. Fiscal policy is run by the central government and works through taxing and spending decisions made in the Union Budget. Monetary policy can change quickly at an MPC meeting; fiscal policy usually moves on the annual Budget cycle.

What is monetary policy in simple terms?

It is how the central bank controls how expensive it is to borrow money and how much money flows through the economy. When the RBI cuts the repo rate, loans get cheaper and people spend more; when it raises the rate, borrowing slows and inflation cools.

Who controls monetary policy in India?

The Reserve Bank of India, through its six-member Monetary Policy Committee (MPC). The committee has three RBI members (including the Governor, who chairs it) and three members appointed by the central government. Decisions are by majority vote, with the Governor holding a casting vote in a tie.

What are the main tools of monetary policy?

The headline tool is the repo rate. Others include the reverse repo / standing deposit facility, the Cash Reserve Ratio (CRR), the Statutory Liquidity Ratio (SLR), open-market operations (buying or selling government bonds), and the marginal standing facility / bank rate.

What is the difference between expansionary and contractionary policy?

Expansionary policy stimulates demand — through lower interest rates (monetary) or lower taxes and higher spending (fiscal) — and is used in slowdowns. Contractionary policy cools demand — through higher rates or higher taxes and lower spending — and is used to fight inflation or repair the deficit.

What is the RBI’s inflation target?

Under the flexible inflation targeting framework, the RBI aims to keep Consumer Price Index (CPI) inflation at 4%, within a tolerance band of plus or minus 2 percentage points — so between 2% and 6%. The target is set by the government in consultation with the RBI and reviewed every five years.

Can monetary and fiscal policy work against each other?

Yes. If the government runs a large deficit to boost demand while the RBI is raising rates to fight inflation, the two policies pull in opposite directions, and the central bank may have to keep rates higher for longer. They are most effective when coordinated, as they were during the COVID-19 response.

Disclaimer: This article is for educational purposes only and is not investment/financial advice. Read all scheme/offer documents and consult a SEBI-registered adviser where relevant.