The fiscal deficit is the gap between what the government spends and what it earns (excluding borrowing) in a year — it shows how much the government must borrow. The current account deficit (CAD) is the gap between the foreign currency India pays out and what it receives on trade, services and income — it shows how much the country as a whole must borrow from the rest of the world. Together these are India’s “twin deficits”: one is the government’s budget shortfall, the other is the nation’s shortfall with foreigners. This guide explains both, how they differ, how they are linked, why they matter to your loans, the rupee and prices, and how each one is financed.

- What is a deficit, in plain English?

- Fiscal deficit: the government’s shortfall

- Current account deficit: the country’s shortfall

- Fiscal deficit vs current account deficit: the difference

- The twin-deficit link: how the two connect

- Why deficits matter to ordinary Indians

- How each deficit is financed

- How India manages its deficits

- FAQ

What is a deficit, in plain English?

A deficit is simply a shortfall — money going out is more than money coming in. The opposite is a surplus (more coming in than going out), and when the two are equal you have a balanced position. The word turns up everywhere in economics, so the important thing is always to ask: whose income and whose spending are we talking about, and over what period?

For a household it is easy. If a family earns ₹50,000 a month and spends ₹60,000, it runs a monthly deficit of ₹10,000 and has to fund the gap — from savings, a credit card or a loan. A persistent deficit means rising debt. The same logic scales up to a government and to an entire country, but the labels change and the consequences are bigger.

India’s two most discussed deficits sit at two very different levels:

- Fiscal deficit — a government measure. It compares the government’s total spending with its total income (excluding borrowing) in a financial year (April–March).

- Current account deficit (CAD) — a whole-economy measure. It compares the foreign-currency money the entire country (government, companies and individuals together) pays to the rest of the world with what it receives, on day-to-day transactions like trade.

Because both carry the word “deficit”, they are easy to mix up. The rest of this guide keeps them firmly apart and then shows where they meet — the famous “twin deficits”.

Fiscal deficit: the government’s shortfall

The fiscal deficit is the difference between the government’s total expenditure and its total receipts excluding borrowings in a year. In one line:

In other words, it is the amount the government has to borrow in a year to meet all its spending. A bigger fiscal deficit means more government borrowing.

What goes into it

The government’s income (the part that is not borrowing) has two buckets:

- Revenue receipts — tax revenue (GST, income tax, corporate tax, customs) and non-tax revenue (dividends from public-sector companies and the RBI, fees, spectrum charges).

- Non-debt capital receipts — mainly money from selling assets, such as disinvestment (selling stakes in public-sector companies) and recovery of loans. These do not create a repayment obligation, so they count as genuine income.

Everything the government spends — salaries, pensions, subsidies, interest on past loans, and capital spending on roads, railways and defence equipment — is its total expenditure. When expenditure is larger than the income above, the shortfall is the fiscal deficit, and it is plugged by borrowing.

It is reported as a percentage of GDP

An absolute rupee figure (lakhs of crores) is hard to compare across years or countries, so the fiscal deficit is almost always quoted as a percentage of GDP (the size of the economy). This is the fiscal deficit to GDP ratio. Expressing it this way answers the real question — how big is the government’s borrowing relative to the economy that has to support it? A ₹1 lakh crore deficit is enormous for a small economy and modest for a large one.

Related deficit terms you will see

The Union Budget reports several deficit measures. They slice the same accounts in different ways:

| Term | Roughly what it measures | Why it is useful |

|---|---|---|

| Fiscal deficit | Total borrowing needed for the year | The headline number; drives government debt |

| Revenue deficit | Shortfall on day-to-day (revenue) account only | Shows borrowing used for consumption, not assets |

| Primary deficit | Fiscal deficit minus interest payments | Strips out old debt to show this year’s fresh gap |

| Effective revenue deficit | Revenue deficit minus grants used to build assets | A cleaner read on “wasteful” revenue spending |

For most readers, fiscal deficit is the one that matters because it determines how much the government adds to its debt pile each year. A high revenue deficit is a warning sign: it means the government is borrowing just to fund running costs (salaries, subsidies, interest) rather than to build lasting assets like infrastructure.

Current account deficit: the country’s shortfall

Step up from the government to the entire country. Every year India deals with the rest of the world — it buys and sells goods, exports software and tourism services, receives money from Indians working abroad, and pays interest and dividends to foreign investors. The record of all these cross-border transactions is the balance of payments, and its most-watched part is the current account.

The current account has four components:

- Trade in goods — exports minus imports of physical products (this gap is the trade deficit). India imports a lot of crude oil, gold and electronics, so this is usually in deficit.

- Trade in services — software (IT), business services, travel and transport. India is a large net exporter of services, which is a big plus.

- Primary income — interest, profit and dividends flowing in and out (mostly out, as foreign investors earn returns here).

- Secondary income (transfers) — chiefly remittances sent home by Indians working overseas. India is among the world’s largest remittance recipients, another big plus.

Why India often runs a current account deficit

India’s current account is a tug-of-war. On one side, a large goods trade deficit — driven heavily by imported crude oil and gold — pulls it into deficit. On the other side, strong services exports (led by IT) and huge remittances pull it back toward balance. When oil prices spike or gold imports surge, the trade deficit widens and the CAD tends to grow; when services and remittances are strong, the CAD shrinks or can even briefly flip to a small surplus.

Fiscal deficit vs current account deficit: the difference

This is the heart of the topic. The two deficits answer completely different questions:

- The fiscal deficit asks: Is the government living within its means? It is about the budget — one player (the government) and its rupee income versus rupee spending.

- The current account deficit asks: Is the country living within its means with the rest of the world? It is about the balance of payments — the whole economy and its foreign-currency earnings versus foreign-currency payments.

A country can have one without the other. You can run a fiscal deficit while running a current account surplus, and vice versa — they are measured on separate ledgers.

| Feature | Fiscal deficit | Current account deficit (CAD) |

|---|---|---|

| Whose gap? | The government’s | The whole country’s (vs the world) |

| What it compares | Govt spending vs govt income (ex-borrowing) | Foreign currency paid out vs received |

| Which account | The Union Budget | The balance of payments |

| Main drivers | Taxes, subsidies, salaries, interest, capex | Oil/gold imports, IT exports, remittances |

| Currency that matters | Mostly rupees | Foreign currency (mainly US dollars) |

| Financed by | Government borrowing (bonds, loans) | Foreign capital (FDI, FPI, external debt) |

| Quoted as | % of GDP | % of GDP |

| Key worry if too high | Rising debt, higher interest costs, crowding out | Pressure on the rupee, drain on forex reserves |

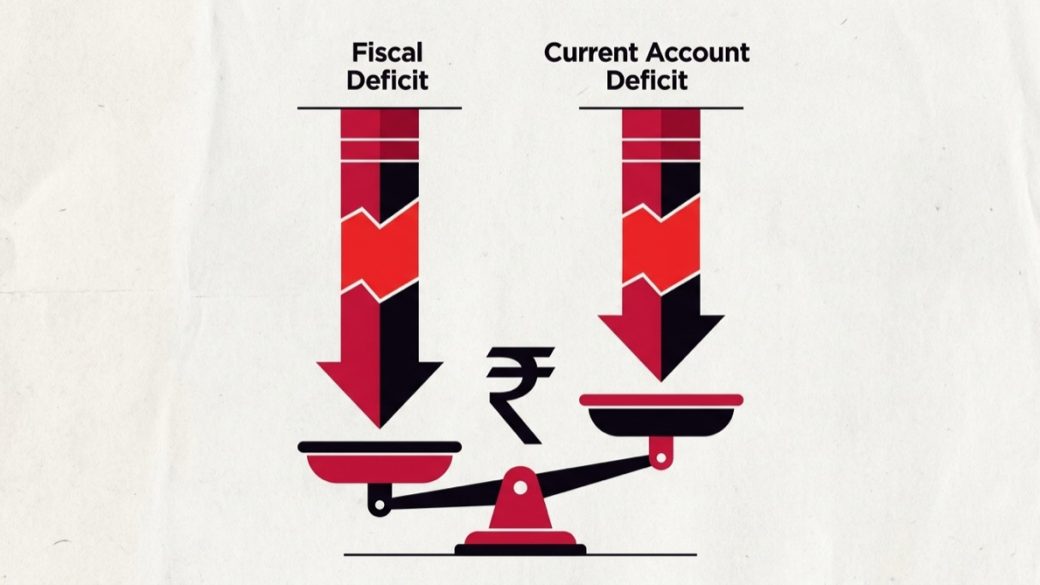

The twin-deficit link: how the two connect

If they are separate, why are they called the twin deficits? Because a large fiscal deficit can spill over into a larger current account deficit. The logic runs like this:

- A big fiscal deficit means the government is injecting a lot of money into the economy — spending more than it taxes.

- That extra spending raises overall demand in the economy. Some of that demand is for imported goods — oil, machinery, electronics, gold.

- More imports widen the trade gap, which widens the current account deficit.

- So, loosely, a government that overspends can pull the whole country into a bigger external gap. Hence “twin” deficits that often move together.

There is a useful identity behind this. In any economy, the current account balance equals national saving minus investment. When the government saves less (runs a bigger fiscal deficit) and that fall is not offset by households and firms saving more, national saving drops — and the current account moves further into deficit. This is why economists watch the two side by side.

Why deficits matter to ordinary Indians

These are not just exam terms — they reach your wallet through interest rates, prices and the value of the rupee.

Why the fiscal deficit matters

- Your loans: heavy government borrowing can push up interest rates for everyone (“crowding out” private borrowers), making home, car and business loans costlier.

- Future taxes and debt: today’s borrowing is tomorrow’s debt. A growing share of the budget then goes just to pay interest, leaving less for schools, health and infrastructure.

- Inflation: if a government finances its gap loosely, too much money can chase too few goods, feeding inflation.

- Ratings and confidence: a credibly controlled fiscal deficit supports India’s sovereign credit rating, which lowers the cost of borrowing for the whole country.

A deficit is not automatically bad. Borrowing to build productive assets — highways, ports, power, railways — can lift growth so much that the economy (and future tax revenue) grows faster than the debt. The danger is borrowing mainly to fund running costs, which is why the quality of the deficit matters as much as its size.

Why the current account deficit matters

- The rupee: a wide CAD means India needs more dollars than it earns, which can weaken the rupee. A weaker rupee makes imports — petrol, diesel, gadgets, foreign education and travel — more expensive.

- Forex reserves: persistent deficits can drain the RBI’s foreign-exchange reserves, India’s buffer against external shocks.

- Vulnerability to global moods: a large CAD must be financed by foreign capital. If global investors turn risk-averse and pull money out, a high-CAD economy is more exposed — the lesson of India’s 2013 “taper tantrum” episode.

Like the fiscal deficit, a modest CAD is normal and even healthy for a fast-growing economy that needs to import capital goods and technology to expand. It becomes a worry only when it is large, persistent and financed by volatile “hot money” rather than stable long-term investment.

How each deficit is financed

A deficit always has a matching source of funding — the gap must be plugged. Where the money comes from is completely different for the two deficits.

Financing the fiscal deficit

The government plugs its gap mainly by borrowing in rupees:

- Dated government securities (G-Secs) and Treasury Bills — bonds sold to banks, insurers, mutual funds, pension funds and, increasingly, foreign investors. This is the largest source.

- Small savings — schemes like PPF, NSC and Sukanya Samriddhi, where public deposits are routed to the government.

- External borrowing — a relatively small share, from institutions like the World Bank and bilateral loans.

Every year’s borrowing adds to total government debt, on which interest must be paid in all future years — which is exactly why a high primary deficit (the gap before interest) is watched so closely.

Financing the current account deficit

A CAD is financed through the capital and financial account of the balance of payments — foreign money flowing into India:

- Foreign Direct Investment (FDI) — long-term investment into factories, companies and projects. The most stable form of financing.

- Foreign Portfolio Investment (FPI) — foreign money in Indian stocks and bonds. Larger and faster, but it can reverse quickly (“hot money”).

- External commercial borrowings (ECBs) — foreign-currency loans raised by Indian companies.

- NRI deposits and other inflows.

If these inflows are more than enough to cover the CAD, the surplus adds to the RBI’s forex reserves; if they fall short, the RBI may sell dollars from reserves to bridge the gap and steady the rupee.

| Question | Fiscal deficit | Current account deficit |

|---|---|---|

| Who borrows? | The government | The country (mostly private + govt) |

| In what currency? | Mainly rupees | Foreign currency (chiefly dollars) |

| Main funding source | G-Secs, T-Bills, small savings | FDI, FPI, ECBs, NRI deposits |

| What it builds up | Government debt | External liabilities to foreigners |

| Safety buffer | Tax base & growth | Forex reserves at the RBI |

How India manages its deficits

The fiscal side: the FRBM framework

India tries to keep the fiscal deficit in check through the Fiscal Responsibility and Budget Management (FRBM) Act, 2003, which commits the government to a path of gradual deficit reduction and greater transparency. In recent years the government has publicly stated a goal of bringing the central fiscal deficit down toward and below 4.5% of GDP, and has signalled an intent to then steer the focus toward bringing down the overall debt-to-GDP ratio. (Always check the latest Union Budget for the figure of the day — targets are revised each year.)

Tools to reduce the fiscal deficit include widening the tax base and improving collection (GST, better compliance), rationalising subsidies, disinvestment of public-sector stakes, and tilting spending toward growth-boosting capital projects.

The external side: the RBI’s toolkit

The current account deficit is managed less by “targets” and more by keeping it financeable and the rupee stable. The RBI and the government use:

- Foreign-exchange reserves — a large buffer (often discussed in terms of how many months of imports it can cover) reassures markets and lets the RBI smooth sharp rupee swings.

- Encouraging stable inflows — easing FDI rules, deepening bond markets (including India’s inclusion in global bond indices), and incentivising remittances and exports.

- Curbing non-essential imports — for example, adjusting duties on gold when the deficit widens.

- Boosting competitiveness — schemes such as Make in India and Production-Linked Incentives aim to cut import dependence and lift exports over time.

Frequently asked questions

What is fiscal deficit in simple words?

The fiscal deficit is the gap between what the government spends and what it earns (not counting money it borrows) in a financial year. In plain terms, it is how much the government has to borrow that year to pay all its bills. It is usually expressed as a percentage of GDP so it can be compared across years and countries.

What is the difference between fiscal deficit and current account deficit?

The fiscal deficit is the government’s budget shortfall — its spending minus its (non-borrowed) income, mostly in rupees. The current account deficit is the whole country’s shortfall with the rest of the world — the foreign currency India pays out minus what it receives on trade, services and income. One is about the Union Budget; the other is about the balance of payments.

Why are they called the twin deficits?

Because they often move together. A large fiscal deficit pumps extra demand into the economy, some of which goes to imports, widening the trade gap and therefore the current account deficit. There is also an accounting link: the current account balance equals national saving minus investment, and a bigger fiscal deficit lowers national saving. It is a strong tendency, not an iron rule.

Is a fiscal deficit always bad?

No. Borrowing to build productive assets like roads, ports and power can lift growth and future tax revenue faster than the debt grows, which is healthy. The deficit becomes a problem when it is large, persistent, and used mainly to fund running costs (salaries, subsidies, interest) rather than to create lasting assets — this is captured by the revenue deficit.

How is the fiscal deficit financed in India?

Mainly by government borrowing in rupees: dated government securities (G-Secs) and Treasury Bills sold to banks, insurers, mutual funds and foreign investors, plus small-savings schemes like PPF and NSC, and a smaller amount of external borrowing. All of it adds to government debt, which carries interest in later years.

How does a current account deficit affect the rupee?

A wide CAD means India needs more foreign currency than it earns, so demand for dollars outstrips supply. That tends to weaken the rupee, which makes imports such as petrol, diesel, electronics and foreign travel more expensive, and can add to inflation. If foreign inflows fall short, the RBI may sell dollars from its reserves to steady the rupee.

What is India’s fiscal deficit target?

Under the FRBM framework the government has publicly aimed to bring the central fiscal deficit down toward and below 4.5% of GDP, after which it has signalled a shift in focus toward reducing the overall debt-to-GDP ratio. The exact target is set and revised in each year’s Union Budget, so check the latest Budget for the current figure.

Disclaimer: This article is for educational purposes only and is not investment/financial advice. Economic figures and government targets change over time — always verify current numbers in the latest Union Budget, RBI releases and official data. Read all scheme/offer documents and consult a SEBI-registered adviser where relevant.