📚 New to this topic? Read our full guide: RBI Repo Rate Explained.

How EPFO Decides Your PF Interest Rate: The Math, Explained Simply

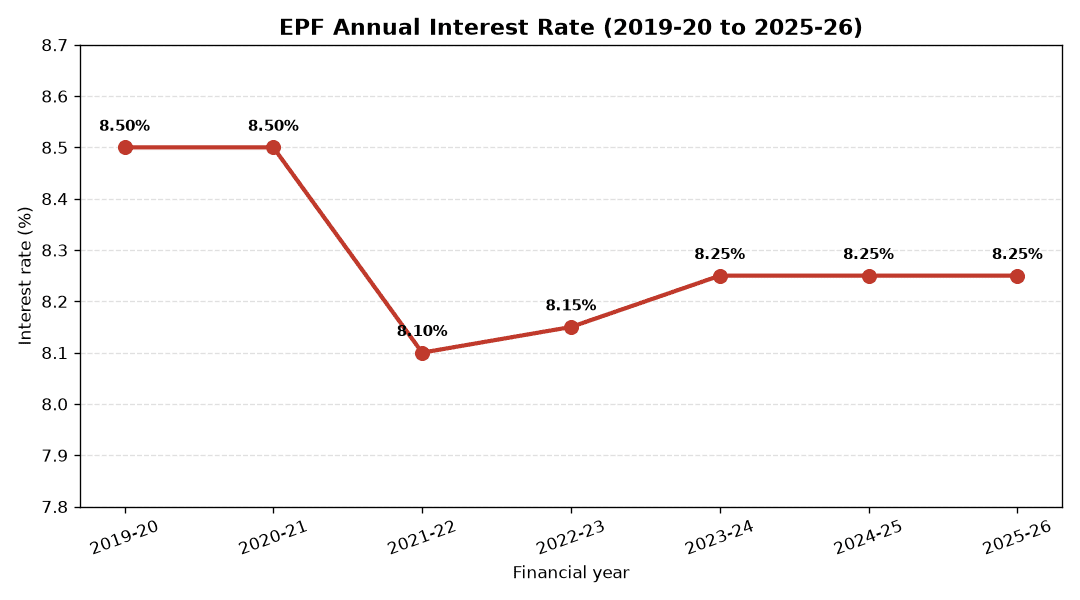

If you have a job in India, a small part of your pay goes into a savings pot each month. This pot is for when you stop working and retire. Once a year, the money in the pot earns interest (extra money paid to you for keeping your savings there). The way this number is worked out sounds hard, but it is not. This article explains how your PF (provident fund, your retirement savings) grows, who picks the rate, and why it matters for you. For 2025-26, the government said yes to an 8.25% rate for about 78 million members. This is the third year in a row at this same rate.

First, the basics: EPF, PF and EPFO in plain words

EPF means Employees’ Provident Fund. It is a savings plan that workers must join. PF is just a short, everyday name for the same thing. Each month, a part of your pay is saved, and your boss puts in money too.

EPFO means the Employees’ Provident Fund Organisation. It is the government group that runs this savings plan. Think of EPFO as the manager of one giant national piggy bank. It holds the money of tens of millions of workers.

You put in 12% of your basic pay plus your dearness allowance (extra pay added to cover the rising cost of living). Your boss puts in a similar amount. Your boss also pays small fees and adds 1% to a linked life-insurance plan (which pays your family money if you die).

Where does the money come from?

The EPFO does not let your money sit and do nothing. It invests the money (uses it to earn more) and pays you interest from what it earns. Each year, new money comes in to invest. This new money is called fresh accretions, which just means fresh cash coming in.

Fresh accretions are made of a few things added together: money put in by workers, interest and dividends earned (dividends are small payments that companies share with the people who own their stock), and money from old investments that have ended and paid back. Then the EPFO takes away the money it had to pay out during the year. In 2024-25 alone, the EPFO got Rs 3,35,629 crore. The biggest part, Rs 2,58,133 crore, came from the workers’ own EPF savings.

Where does EPFO invest your PF money?

The EPFO follows an investment pattern set by the Ministry of Labour and Employment. This pattern is a rulebook. It says how much money can go into each kind of investment. Most of the money goes into safe debt. Debt here means lending money to the government and to companies, who then pay it back with fixed interest.

Under its 2024-25 rules, the new money is split like this: 45-65% can go into government securities (loans to the government), 20-45% into other debt, up to 5% into short-term debt, 5-15% into equities (shares, which are small parts of a company that you own), and up to 5% into other special types. The share part is bought through ETFs. An ETF (exchange-traded fund) is a basket of many shares. You can buy and sell the whole basket like one single stock.

By March 2025, the EPFO’s total pot of investments was a huge Rs 28,37,054 crore. Most of it is in loans to the central and state governments. About 10% is in ETFs, and about 20% is in corporate bonds (loans to companies).

So how is the interest rate actually decided?

Here are the simple steps:

- The EPFO adds up all the money it earned from its investments during the year.

- It checks how much it must pay out. It tries to keep a small surplus (extra cash left over) for a rainy day.

- The Central Board of Trustees (CBT), the top group that makes decisions for the EPFO, suggests a rate.

- The Finance Ministry says yes to it (this is called ratifying it).

- Only then is the interest added to your account.

The interest is added once a year. But it is worked out on your monthly running balance (how much money is in your account each month). So money that stays in your account for more months earns more.

Why the rate goes up and down

The rate depends on how much the EPFO earns. When its investments do well, it can pay more. When it earns less, the rate may drop. For 2025-26, the EPFO kept the rate at 8.25%, but the math was tight (there was not much money to spare).

In fact, the EPFO is thought to have made a loss of about Rs 944.06 crore on its interest payouts in 2025-26. This is based on talks at the March CBT meeting, as reported by The Indian Express. A slightly lower rate of 8.10% would have left extra cash of Rs 1,675.82 crore instead. In 2024-25, the extra cash left over was a healthy Rs 5,480.34 crore. So keeping the rate the same came at a cost.

Key facts at a glance

| Item | Figure |

|---|---|

| EPF interest rate for 2025-26 | 8.25% |

| Members covered | About 78 million |

| Years rate held at 8.25% | 3 in a row |

| Total income received (2024-25) | Rs 3,35,629 crore |

| Member EPF contributions (2024-25) | Rs 2,58,133 crore |

| Total investment corpus (Mar 2025) | Rs 28,37,054 crore |

| Estimated payout loss (2025-26) | Rs 944.06 crore |

| Surplus (2024-25) | Rs 5,480.34 crore |

Who manages all this money?

The CBT keeps a close watch. But expert fund managers do the day-to-day work of investing. UTI Asset Management and SBI Fund Management look after the debt portfolio (all the loan investments grouped together). Their work is checked against a benchmark (a target return they must try to beat) set by the ratings firm Crisil. In 2024-25, the debt yield (the return earned from the loans) was 7.33%, just above the 7.30% target.

For shares, the EPFO started by investing 5% of its pot through ETFs in August 2015. It then raised this to 15% of the fresh money from 2017. Since July 2023, Nippon Life India AMC and ICICI Prudential AMC also help manage the share money.

Why it matters, especially for India and young earners

For most salaried Indians, EPF is the biggest part of their retirement savings. An 8.25% return that is mostly tax-free is hard to beat among safe options that pay fixed returns. Over 30 years of work, a steady rate can turn small monthly cuts from your pay into a big retirement corpus (your total pot of savings).

But the 2025-26 loss is a warning sign. If the EPFO keeps paying out more than it earns, it eats into its safety cushion. That could force a lower rate in the years ahead. For founders and business owners who cut PF for their staff, knowing this math helps you explain pay and benefits clearly to your team. Money decisions like these sit next to other big steps on worker pay this year, such as the deferred 8th Pay Commission pay fixation. Ups and downs in the market matter too, as seen in how PMS client numbers fell amid volatility.

FAQ

How often does the EPF interest rate change?

It is checked every financial year. The rate can go up, go down, or stay the same. It depends on how much the EPFO earns from its investments.

Is EPF interest credited monthly or yearly?

The interest is worked out on your monthly running balance. But it is added to your account once a year, after the government says yes to the rate.

Can the rate fall in future?

Yes. The 2025-26 rate came with an expected loss on payouts. If the EPFO earns less, or its extra cash shrinks too far, it may have to lower the rate.

The takeaway

The EPF interest rate is not a random number. It is the result of careful math: money earned from investments, minus money paid out, with a small buffer kept aside, then signed off by the government. Right now the rate is good at 8.25%. But the thin margins of 2025-26 show we cannot take it for granted. Keep an eye on it, because it shapes how big your retirement pot grows.

Source: The Financial Express.