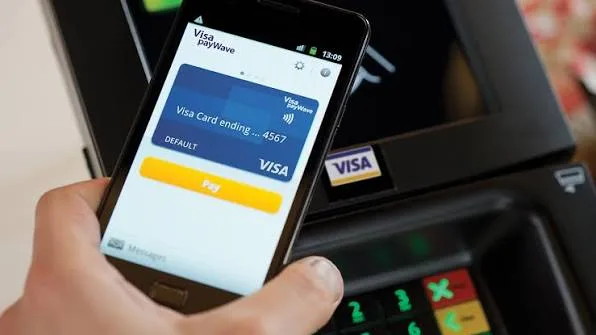

Card tokenisation India is now a global leader in safer online card payments, according to Visa. Card tokenisation India means your real card number gets replaced with a hidden digital code. That helps block fraud because shops do not store your actual card details. Visa says more than 70% of its e-commerce card payments in India now use tokens.

Key takeaways

- Visa says India is now its most tokenised market for online card payments.

- More than 70% of Visa e-commerce transactions in India use tokens.

- A token is a substitute code, so merchants do not keep your real card number.

- The RBI pushed token use after banning merchants from storing card data in 2022.

- More token use can cut fraud and make repeat online checkout faster.

Why is card tokenisation India suddenly a big story?

Because this is not just a payments tech update. It shows how fast India changed the way people pay online. A few years ago, many websites stored your card number. That made checkouts easy, but it also created a big risk if those systems were hacked.

Then the Reserve Bank of India, or RBI, stepped in. The RBI is India’s central bank. It told merchants and payment firms to stop storing full card details and move to token systems instead. That rule reshaped online payments across apps, travel sites, food delivery platforms, and shopping stores.

Visa now says India has become the world’s most tokenised market for online card payments on its network. That matters because Visa is one of the biggest card companies on Earth. If India leads even on Visa’s global map, it means the shift here has been huge.

What is card tokenisation India, in simple words?

Think of your card number like the key to your house. You would not want every shop to keep a copy. Tokenisation solves that problem by giving each merchant a stand-in code instead of the real number.

That stand-in code is called a token. A token is a random digital string linked to your card. If a hacker steals the token from one shop, it is far less useful than stealing the full card number. In many cases, it works only for that card, that merchant, and that device.

So when you save your card on an app, the app may now save a token, not the real card details. That makes repeat payments smoother, but also safer. It is one of those rare changes where convenience and security can improve together.

How big is the shift in numbers?

Visa said over 70% of its e-commerce card payments in India are now tokenised. That is the headline number. It means more than 7 out of every 10 online Visa card transactions in India use tokens.

India also has a massive digital payments base, so even a percentage point means a lot. The country processes billions of online purchases each year across cards, UPI, wallets, and net banking. Cards are only one piece of that mix, but they remain important for big-ticket shopping, travel, and subscriptions.

Here is a simple snapshot of the key figures mentioned in the story and policy background.

| Metric | Figure | Why it matters |

|---|---|---|

| Visa e-commerce card payments in India using tokens | 70%+ | Shows very wide adoption |

| Online payments represented by that share | 7 in 10 | Easy way to picture the scale |

| Year RBI card-on-file tokenisation rules kicked in | 2022 | Policy trigger for the shift |

Visa India e-commerce paymentsTokenised share70%+Non-tokenised shareunder 30%

Why did India move so fast on this?

The biggest reason is regulation. Regulation means rules set by authorities. In India, the RBI forced the market to change after concerns around card data storage and fraud risk.

When businesses could no longer keep full card details, they had to adopt token systems or lose easy repeat payments. That created a strong push across banks, card networks, payment gateways, and merchants. A payment gateway is the service that carries payment data between a website, a bank, and a card network.

India also had the right setup for quick adoption. People already use digital apps for shopping, food, travel, and bills. So once large platforms added tokenised card storage, millions of users moved with them.

Another factor is habit. Indian consumers are used to security steps like OTPs. OTP means one-time password. Since users already expect an extra layer of safety, tokenisation fit into the system without feeling too strange.

What does this mean for shoppers and businesses?

For shoppers, the clearest benefit is safety. If a merchant gets hacked, your real card number is less likely to leak. That does not stop every kind of fraud, but it reduces one major risk.

It can also make repeat checkout faster. You may still see your saved card on a shopping app, even though the app does not keep the actual number. That helps businesses too, because fewer steps at checkout can mean fewer abandoned carts.

For banks and networks, tokenisation can improve trust. If people feel safer, they are more willing to pay online with cards. That is useful in a country where many payment methods compete hard for each transaction.

Businesses, however, had to do real work to get here. They had to update systems, work with card networks, and explain changes to users. That is similar to how other parts of India’s payment system have changed under policy pressure, such as moves affecting digital platform payments and GST on ride-hailing apps.

Does this change India’s wider digital payments story?

Yes, though it does not replace UPI. UPI is India’s instant bank-to-bank payment system. It dominates daily small payments, but cards still matter for online shopping, hotel bookings, airline tickets, and subscriptions.

That means card tokenisation India adds another layer to the country’s broader payments rise. India is building systems that are fast, cheap, and safer at the same time. We have seen similar policy-led shifts in energy, trade, and finance too, from plans to cut natural gas imports using biogas to the wider push around India-US trade deal talks.

There is also a global signal here. Many countries talk about safer digital payments, but India turned that into large-scale action. Because the market is big and fast-moving, companies often treat India as a test bed for payment changes that may spread elsewhere.

India’s rise in tokenised card payments shows that a strict rule can change everyday tech fast. In plain terms, online merchants stopped keeping real card numbers, and millions of shoppers shifted to safer saved-card payments.

Where did the numbers come from?

The headline figure came from Visa, which shared that India is now its most tokenised market for online card payments. You can read more from Visa and the policy background from the Reserve Bank of India. Primary sources matter because they show where the rule came from and who measured the payment trend.

It is also smart to remember what the claim means. Visa’s statement reflects activity on Visa’s network, not every payment in India. Still, Visa is large enough that the trend tells us something real about the market.

What should you watch next?

First, watch whether tokenisation spreads even deeper into subscriptions and recurring payments. Recurring payments are charges that repeat, like video streaming or gym fees. Those are places where saved cards really matter.

Second, watch fraud trends. If tokenisation works as expected, card data theft should become less rewarding for criminals. Fraud never disappears fully, but smarter systems can make attacks harder and less useful.

Third, watch how other networks talk about India. If Mastercard, RuPay, and payment firms report similar patterns, the case gets stronger. Then this will not just be a Visa milestone. It will be a sign that India has changed the rules of online card safety at scale.

FAQs

What is card tokenisation?

It replaces your real card number with a digital code. That code is used for payments, so merchants do not store the actual number.

Why is card tokenisation India important?

Because India is a huge online payments market. If token use crosses 70%, it shows safer payments can scale very fast.

Who pushed this change in India?

The RBI drove the change with card data storage rules in 2022. Banks, card networks, and merchants then built the systems to follow those rules.