Accelerating its historic pivot away from Western fiat currencies, the People’s Bank of China (PBOC) expanded its official gold reserves by approximately 9.95 tonnes (320,000 troy ounces) in May 2026.

According to data released by the State Administration of Foreign Exchange (SAFE), the acquisition marks the 19th consecutive month of continuous gold accumulation by the Chinese central bank. This buying spree breaks the country’s previous 18-month record set between late 2022 and early 2024, bringing China’s total sovereign gold holdings to a staggering 2,331.5 tonnes (74.96 million ounces).

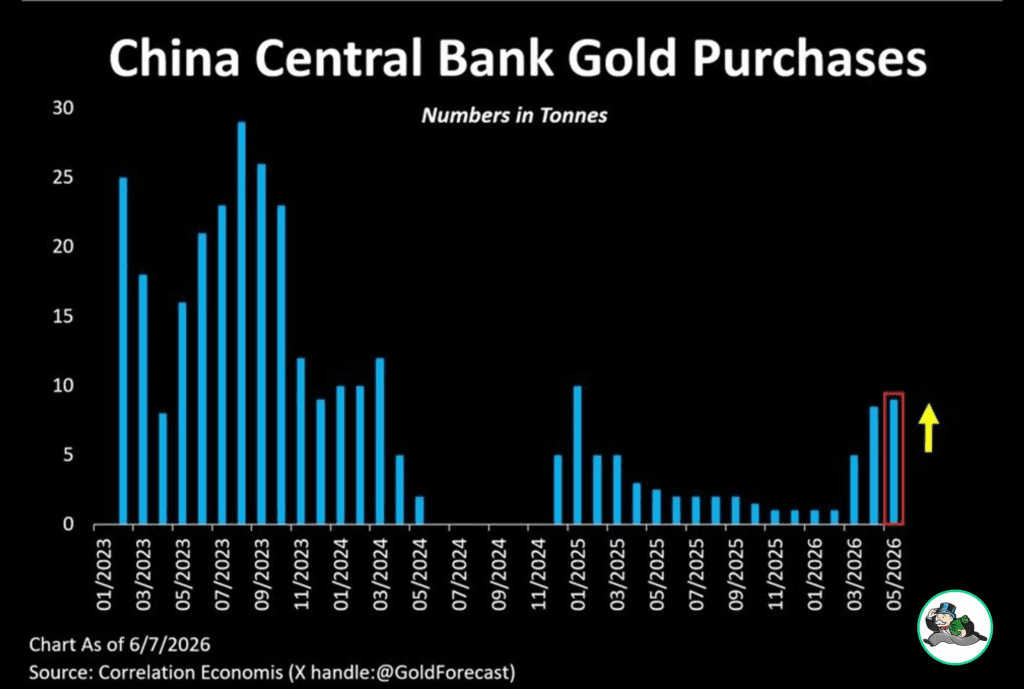

Shifting Gears: Acceleration Amid Dropping Prices

The PBOC’s buying patterns over the past few months reveal an aggressive scale-up in volume. After a brief period of highly conservative, low-tonnage buying early in the year, China’s reserve managers have significantly stepped up their acquisition intensity over the last three months:

- March 2026: +160,000 ounces (~5 tonnes)

- April 2026: +260,000 ounces (~8 tonnes)

- May 2026: +320,000 ounces (~9.95 tonnes)

Market analysts point out that the May acceleration was highly strategic, timed to capitalize on a recent pullback in global spot prices. Gold dipped to an intra-year floor near $4,170–$4,330 per troy ounce in late spring, weighed down by persistent global inflation prints and hawkish signals from Western central banks. For the PBOC, which utilizes a long-term cost-averaging strategy, this price correction presented a premier buying window.

De-Dollarization and the New Reserve Reality

The overarching driver behind China’s insatiable appetite for gold is structural, not speculative. Following the sweeping immobilization of Russian central bank assets by Western nations in 2022, emerging economies have systematically reworked their risk models regarding offshore, single-currency dependencies.

The broader geopolitical impact of this strategy is now hitting a critical macro threshold:

- Gold Flips U.S. Debt: According to recent data from the European Central Bank, gold officially accounted for 27% of global official reserve assets by the end of 2025, while the share of U.S. Treasury bonds fell to 22%. This marks the first time in modern history that gold has surpassed U.S. government debt as the largest component of global central bank reserves.

- The Valuation Runway: Even with 2,332 tonnes in its vaults, gold still only constitutes roughly 8.8% to 9% of China’s massive $3.44 trillion foreign exchange reserves. When compared to the United States or Germany—where gold makes up over 65% of national reserves—the PBOC still has massive structural runway to continue its buying program for years to come.

SEO & Financial Market Impacts: What it Means for Investors

For macroeconomic observers, commodities traders, and financial content publishers, China’s continuous accumulation establishes a rock-solid floor underneath the metals market.

1. Re-Anchoring the Long-Term Gold Floor

While short-term retail sentiment has cooled slightly in recent weeks, the aggressive presence of a massive, price-sensitive institutional buyer like the PBOC prevents deep market sell-offs. Major banking entities like Goldman Sachs have maintained an aggressive year-end 2026 price target of $5,400 per troy ounce, citing central bank demand as a primary pillar.

2. The Export Surplus Flow

China’s capacity to continue this massive buying program stems directly from its booming trade numbers. SAFE’s data shows China’s total foreign exchange reserves climbed to a multi-year high of $3.442 trillion at the end of May, driven heavily by an explosive surge in foreign trade and industrial exports. This massive cash cushion gives the PBOC unparalleled policy space to treat gold as a strategic, long-term resource.

3. A Blueprint for Global Reserve Asset Portfolios

China is not operating in a vacuum. Central banks across Eastern Europe, India, and the Middle East are mirroring this asset allocation strategy. As financial platforms and corporate treasuries look to hedge against a highly fragmented geopolitical landscape, physical gold is increasingly being treated as the ultimate, sanction-proof store of value—a macro narrative that will continue to dominate global economic headlines throughout the rest of 2026.