{kind=link}

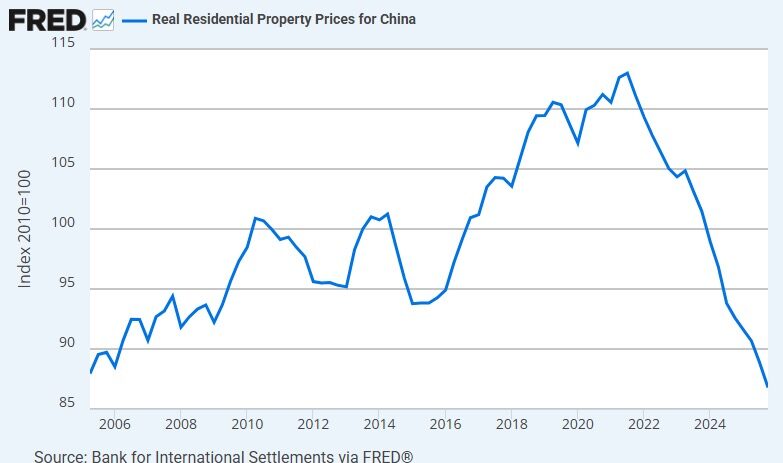

Reports from Tuesday, April 28, 2026, confirm that China’s property market has hit a staggering 20-year low, as measured by the 70-city price index. This “slow-motion collapse” has now persisted for four consecutive years, erasing nearly a quarter of the market’s value in inflation-adjusted terms since its 2021 peak.

The downturn has fundamentally shifted China’s economic outlook, with analysts warning that the real estate sector—once responsible for 25% of GDP—is now a structural drag on growth.

1. Market Data: The 20-Year Trough

According to the National Bureau of Statistics and the Bank for International Settlements, the decline has accelerated in the first half of 2026.

| Metric | Status (April 2026) | Historical Context |

| Price Index | 86.79 | Lowest since 2005 (down from 113 in 2021). |

| New Home Sales | -6.2% (Proj. FY26) | Sixth consecutive year of decline. |

| Unsold Inventory | 391 Million sq. m. | Up 72% since 2021; primarily completed but vacant. |

| RE Investment | -11% YoY | Developers are pivoting to maintenance over new builds. |

- Wealth Erasure: Unlike Western economies where wealth is diversified in equities, approximately 70% of Chinese household wealth is tied to real estate. The 20-year low in prices represents a massive destruction of middle-class net worth.

- GDP Fallout: Prediction markets for China’s 2026 GDP growth have shifted significantly, with many traders now betting on growth falling below 1.0% due to the property sector’s drag.

2. Corporate Collapse & the “White List”

The crisis has moved from smaller developers to the industry’s most established names.

- Evergrande & Country Garden: Following their 2024–2025 collapses, these firms are undergoing liquidation. Evergrande was officially delisted from the Hong Kong Stock Exchange in August 2025.

- Vanke’s Struggle: Long considered the most stable private developer, Vanke reported a record $6.8 billion loss for 2024 and spent early 2026 seeking debt extensions.

- The “White List” Strategy: Beijing is doubling down on its “White List” mechanism, where specific viable projects receive state-backed funding to ensure completion, even if the parent developer is insolvent.

3. Government Stabilization Plan (2026)

In response to the 20-year low, the Politburo and the People’s Bank of China (PBOC) have outlined a “New Development Model” for the sector:

- Inventory Buybacks: Local governments are being encouraged to purchase unsold commercial housing and convert them into affordable rental housing.

- Phasing out Pre-Sales: The government is signaling an end to the “high-leverage” pre-sale model (where buyers pay for unbuilt homes), moving toward a “sold-upon-completion” system to restore buyer trust.

- Monetary Easing: On April 20, 2026, the PBOC issued another 10bp rate cut specifically targeting mortgages to lower the barrier for first-time buyers.

4. Is the Bottom in?

While some analysts (including those from JPMorgan) suggest that prices in Tier-1 cities like Beijing and Shanghai showed early signs of “troughing” in March 2026, the secondary market in Tier-3 and Tier-4 cities continues to plummet.

- The Bear Case: S&P Global warns that nationwide sales volume will likely shrink another 4–5% through the remainder of 2026 as “upgraders” struggle to sell their existing homes in a glutted market.

- The Bull Case: A “wealth effect” from a recent rebound in Chinese equities (up 4% in April) could eventually spill over into housing demand, provided consumer confidence stabilizes.